Welcome to the March edition of the Motive Monthly Economic Report. What follows is an analysis of the major trends in the supply chain and economy across the Motive platform during the past month. Keep reading for a front-seat view into key factors currently influencing the U.S. economy.

Big picture: February brings mixed results for market contraction and retail demand

- February brought mixed signals for the US freight market, as both new carrier registrations and carrier exits increased.

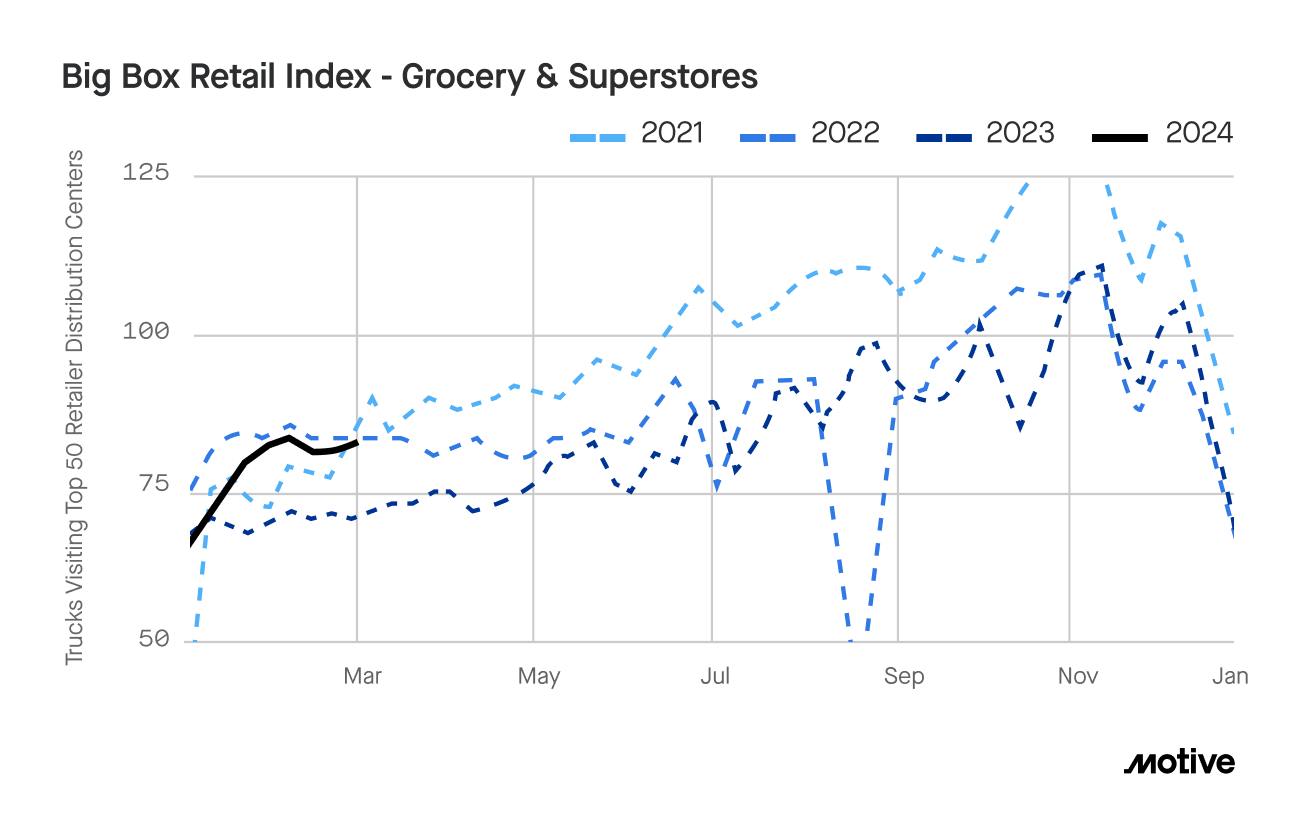

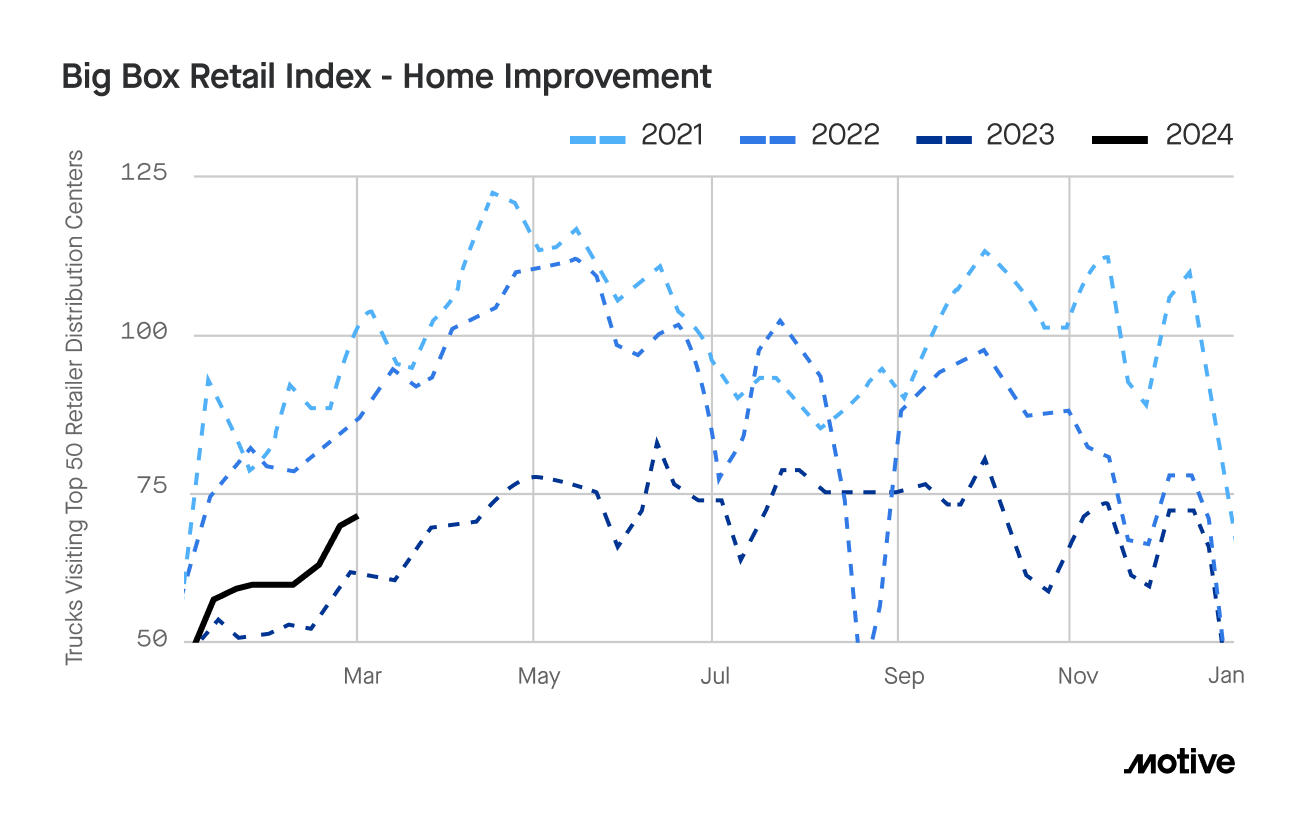

- Motive’s Big Box Retail Index saw another 1.2% increase, with grocery, superstore, non-durables, and home improvement retailers seeing the biggest gains. We anticipate these trends will maintain in 2024, with home improvement, in particular, outperforming compared to last year.

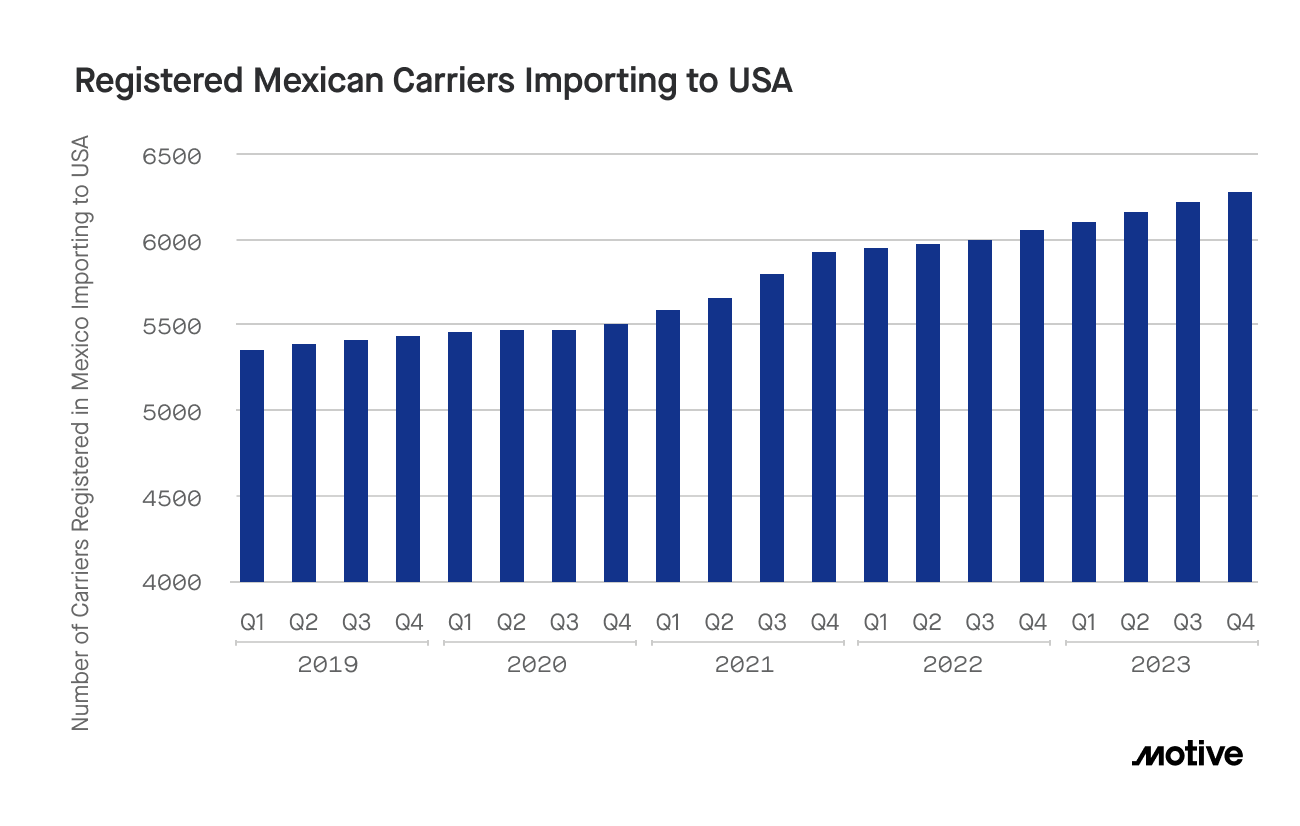

- Mexican carriers importing US goods see significant growth as nearshoring continues to ramp up.

- Motive predicts that sustained consumer demand and improved spot rates will create a more carrier-friendly environment starting in Q3 2024.

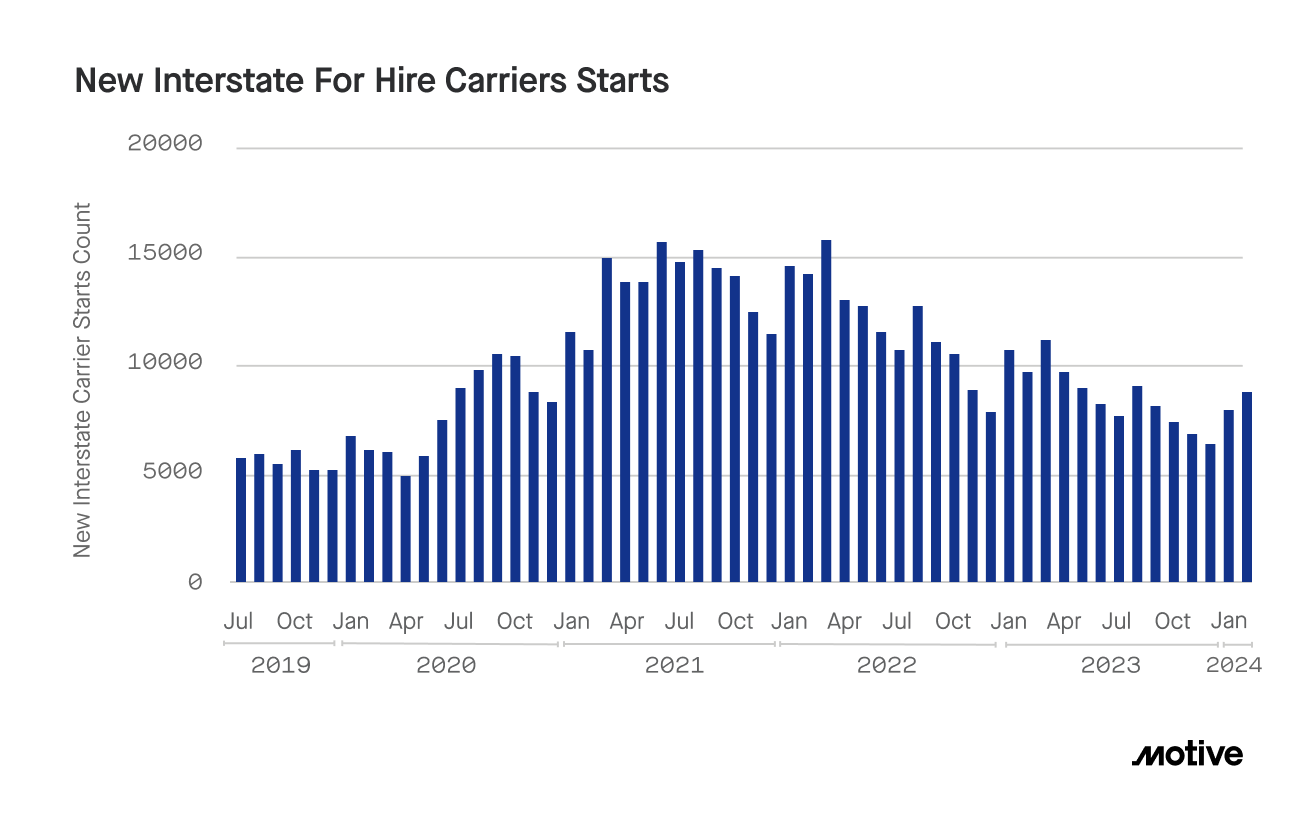

New carrier entries point to shifts in the trucking market; be ready to take advantage of it

The entrance of new carriers (both from within the US and abroad) into the trucking market in 2024 reveals a vastly changed landscape compared to 2019. Influenced by the global pandemic, the US economy has experienced fluctuations in demand as well as periods of growth, decline, and gradual recovery.

New routes for importing goods into the US are emerging. Predicting future market dynamics can be challenging, but these shifts provide an opportunity for established carriers to navigate the recovering market. They can capitalize on promising trends such as the potential for increases in rates and demand, as well as prepare for challenges like rising operational costs.

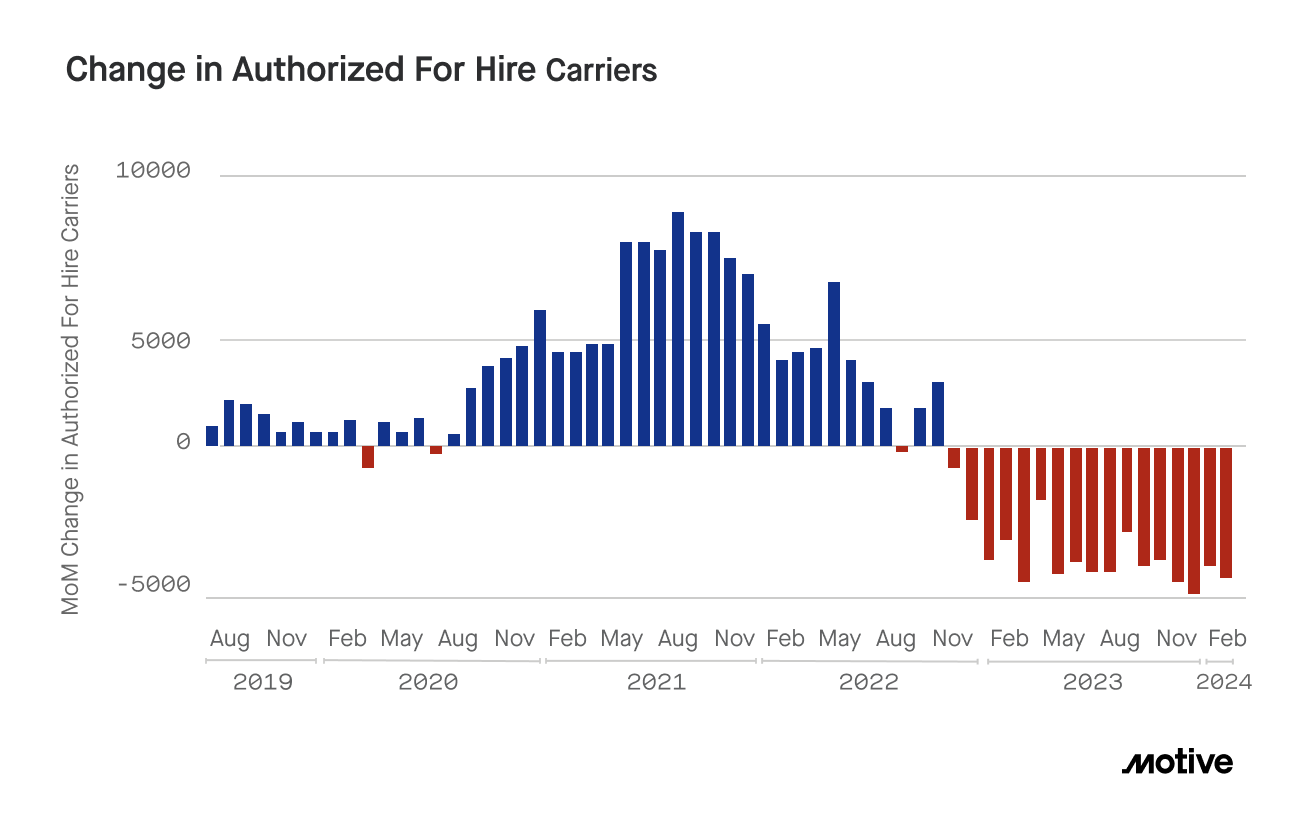

February presented a complex scenario for the US trucking market, as both new carrier registrations and carrier exits increase

The industry saw a departure of more than 4,000 carriers, a 10.3% increase from the previous month. This is likely due to spot market prices remaining at unprecedented lows, which exacerbated business closures.

Conversely, the month also saw a 9% increase in new carrier registrations, totaling 8,675, despite being 11% lower than the same period last year. This growth, building on January’s positive trend, suggests a cautious optimism among new entrants. Analysts anticipate rate improvements throughout the year, which seems to be encouraging the steady rise in new carrier registrations.

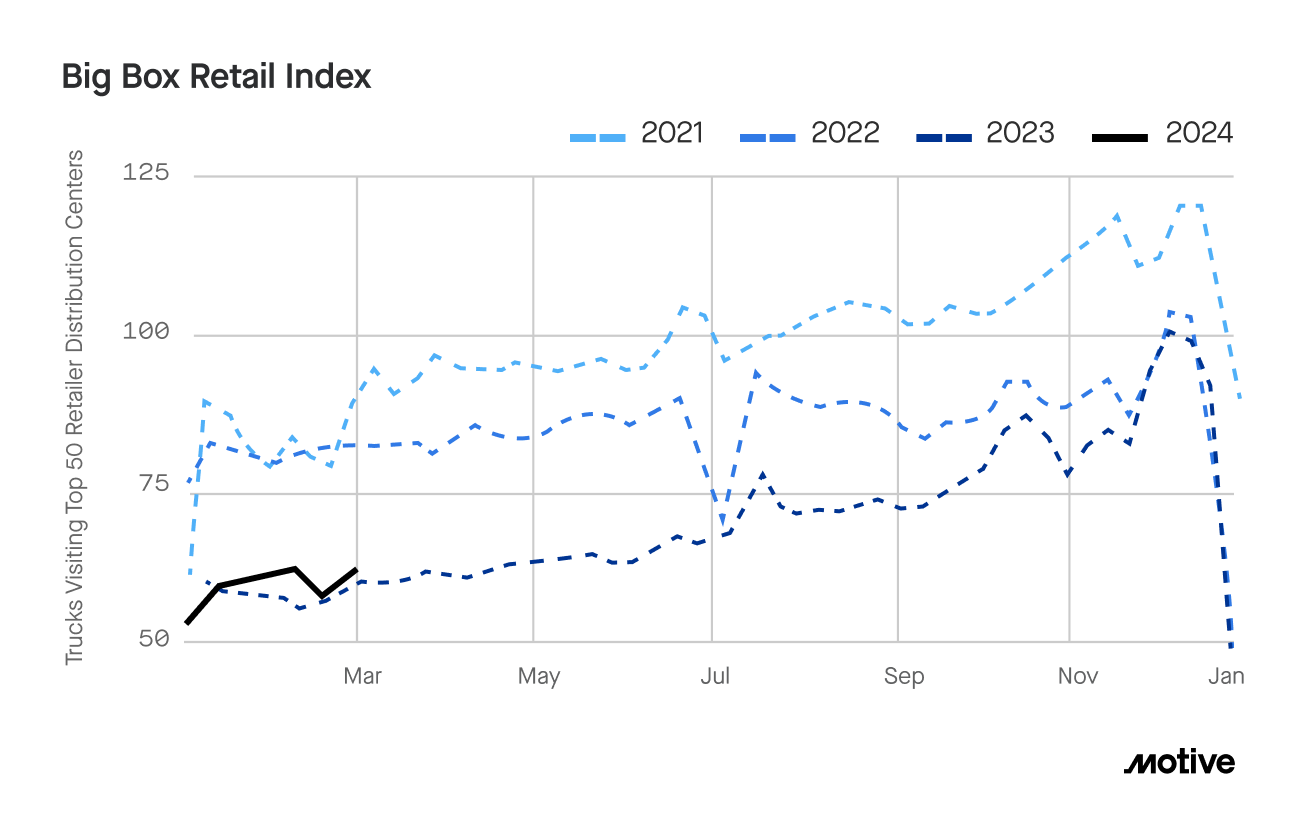

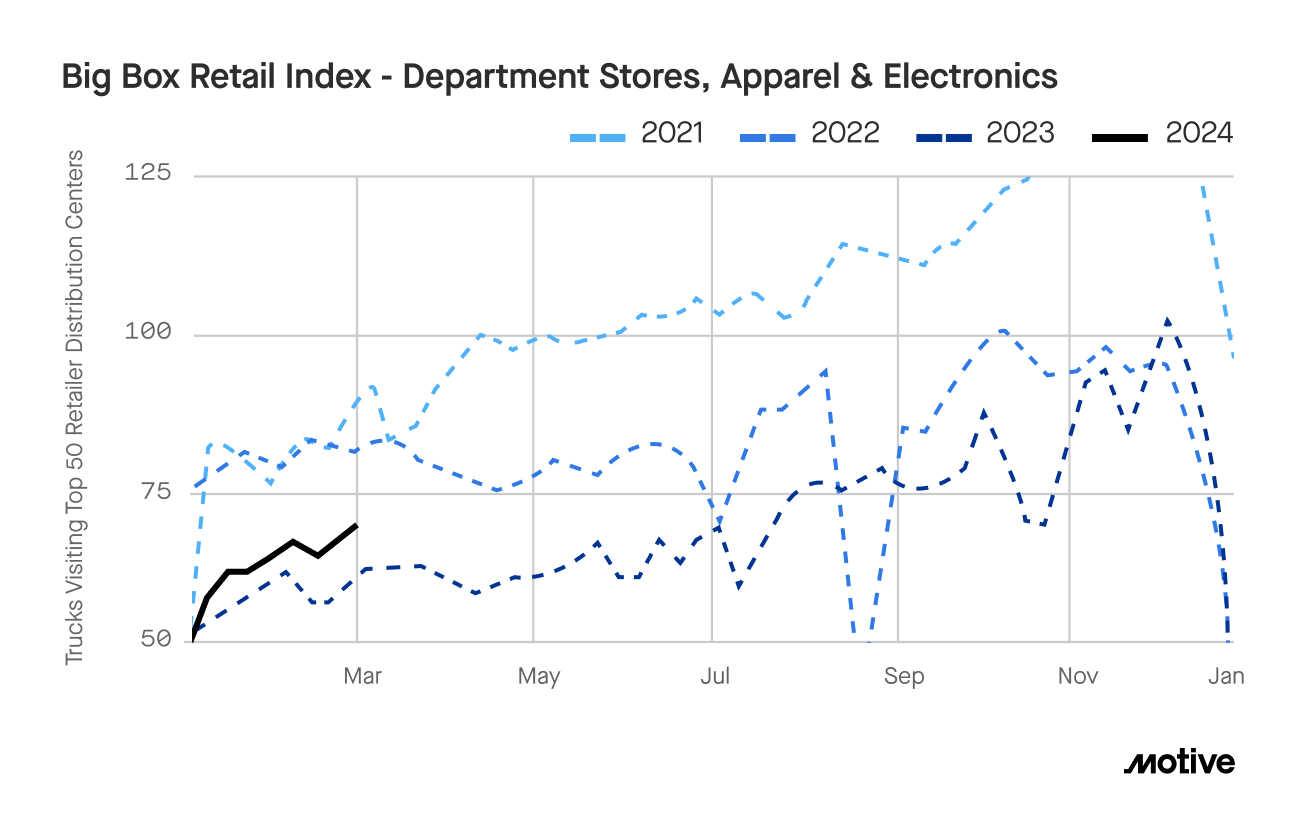

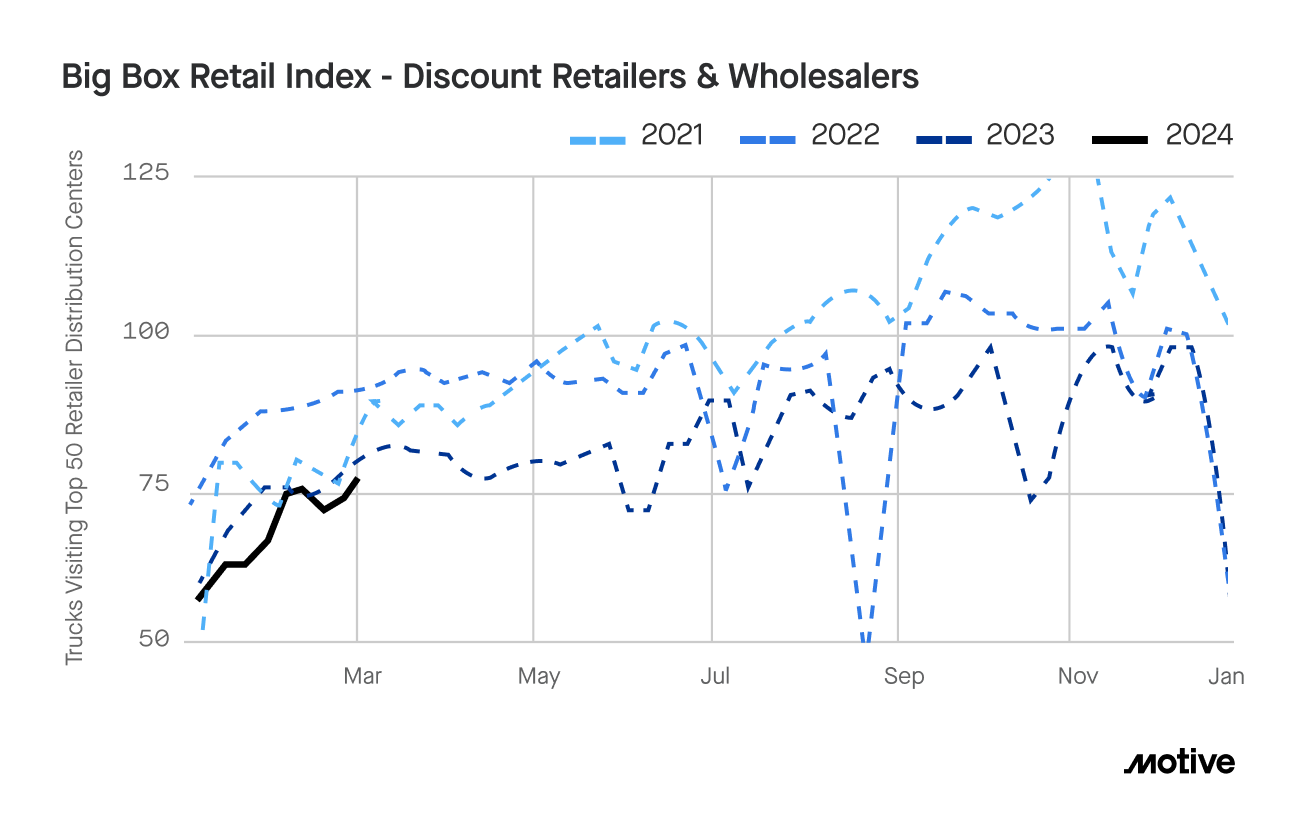

In February, visits to the top 50 retail warehouses saw a modest increase, with grocery, superstore, and home improvement categories experiencing a significant surge

Top 50 retailer warehouses saw a 1.2% increase in trucking visits in February as retail demand across e-commerce and major brick-and-mortar stores tracked 2023 levels.

While this week brought news of rising consumer prices, generally positive consumer sentiment appears to be driving sustained demand for big box retailers. Motive’s Big Box Retail Index saw visits to warehouses for the top 50 retailers increase 1.2% in February as demand across e-commerce and major brick-and-mortar stores tracked 2023 levels. Sectors seeing significant surges included department stores, apparel and electronics (15.6% YoY), home improvement stores (14.6% YoY), and grocery and superstores (12.1% YoY). In contrast, discount retailers and wholesalers saw a steeper decrease compared to January (4.5% YoY). We anticipate these trends will maintain in 2024, with home improvement outperforming last year.

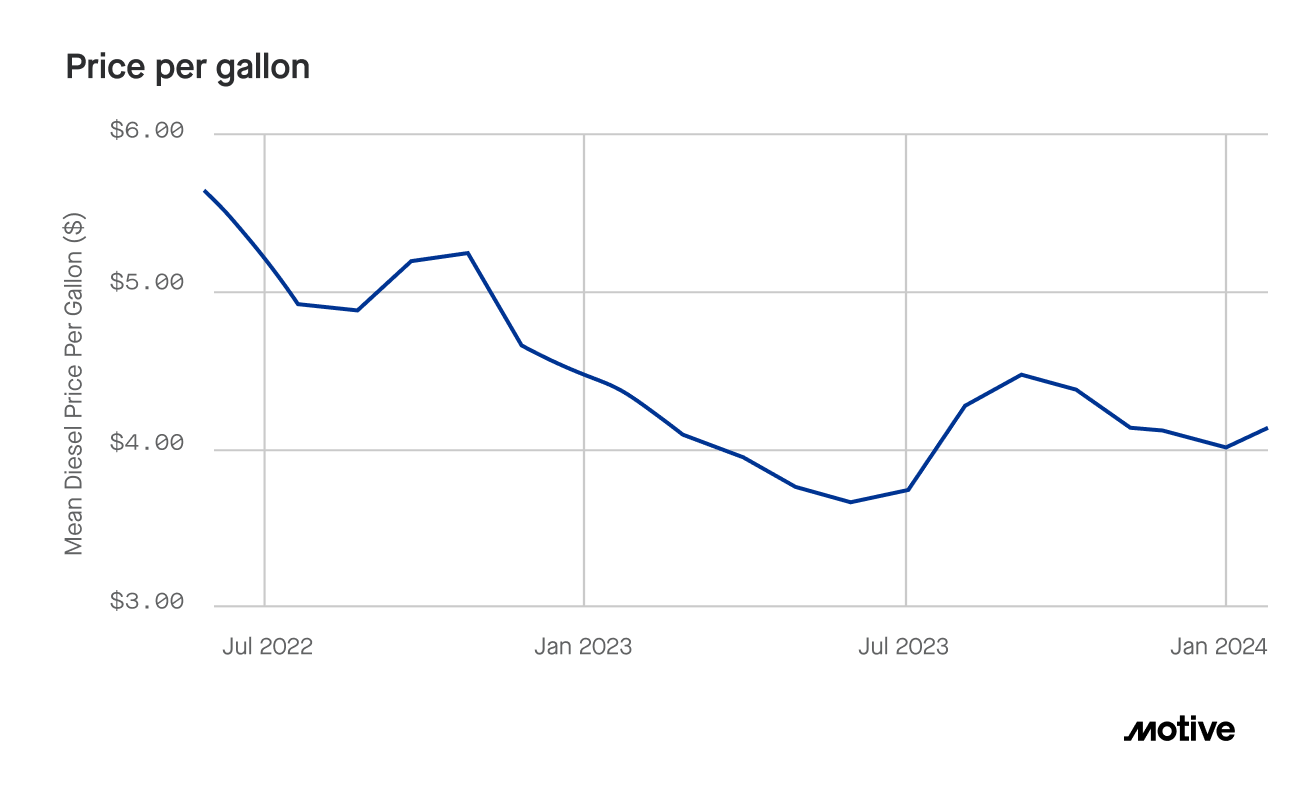

Meanwhile, diesel prices reversed their recent decline, rising 3.1% month over month. In addition to international factors, recent weather-related disruptions and outages seem to have contributed to domestic production slowing and prices increasing.

Mexican carriers importing US goods see significant growth as nearshoring continues to ramp up

As Motive CEO Shoaib Makani recently noted, the trend of moving production away from Asia has gained momentum, with a focus on both offshoring and onshoring strategies. Mexican carriers importing US goods have been some of the biggest beneficiaries of this, as the number of vehicles registered for cross-border shipping grew by 14.3% and the average fleet size grew by 11.3% in 2023. The market’s overall growth was 2.3%, compared to a US trucking market that saw a 6.6% contraction.

As consumer demand recovers in 2024 and more carriers and retailers invest resources in and around Mexico, this trend shows no signs of slowing down. Companies will continue to look to production and logistics in Mexico as a hedge against challenges to intercontinental shipping (such as ongoing international tensions).

Motive’s prediction: Consumer demand and improvement in rates will create a more carrier-friendly market in 2H24

Motive predicts that by the second half of 2024, we will be in a more carrier-friendly environment. February data supported last month’s prediction that 2024 carrier registrations would outpace pre-pandemic levels by 10-20%. Meanwhile, sustained consumer demand, normalized restocking patterns, and potential improvement in spot rates show further positive signals for the trucking market. We anticipate rates will have moved upward and consumer demand will keep its current pace in the second half of 2024, leading to fewer carrier exits in addition to the previously mentioned gains in net-new registrations.

Data Methodology

The Motive Monthly Economic Report uses aggregated and anonymized insights from the Motive network, as well as publicly available government data from the Federal Motor Carrier Safety Administration, U.S. Census, and U.S. Department of Transportation.