Welcome to the June edition of the Motive Monthly Economic Report. What follows is an analysis of the major trends in the supply chain and economy across the Motive platform of 100,000 customers during the past month. Motive’s transportation and logistics data is a reflection of consumer demand and therefore, a leading indicator of overall economic stability and trends. Keep reading for a front-seat view into key factors currently influencing the U.S. economy.

Motive Predictions:

- Higher freight-per-mile rates in peak season will squeeze the bottom lines of retailers and give carriers more leverage in Q4, early 2025.

- While the effect won’t be immediate, higher rates will cause further increases in consumer prices by Q2 2025.

- The entire supply chain will get more expensive, and many retailers need to rethink their low-inventory restocking strategies.

- Trucking and logistics jobs will climb significantly by the end of the year as Q3 will bring the first net-positive growth of the trucking market since 2022.

Retailer restocking demand remains strong, but rising rates will flip the supply chain power dynamic.

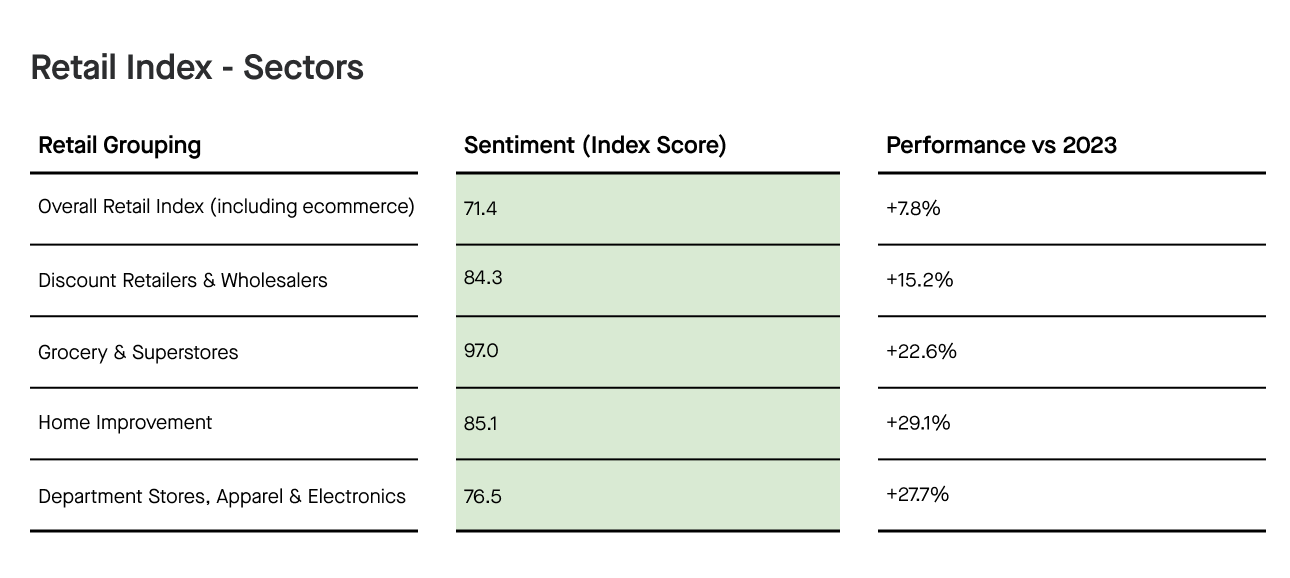

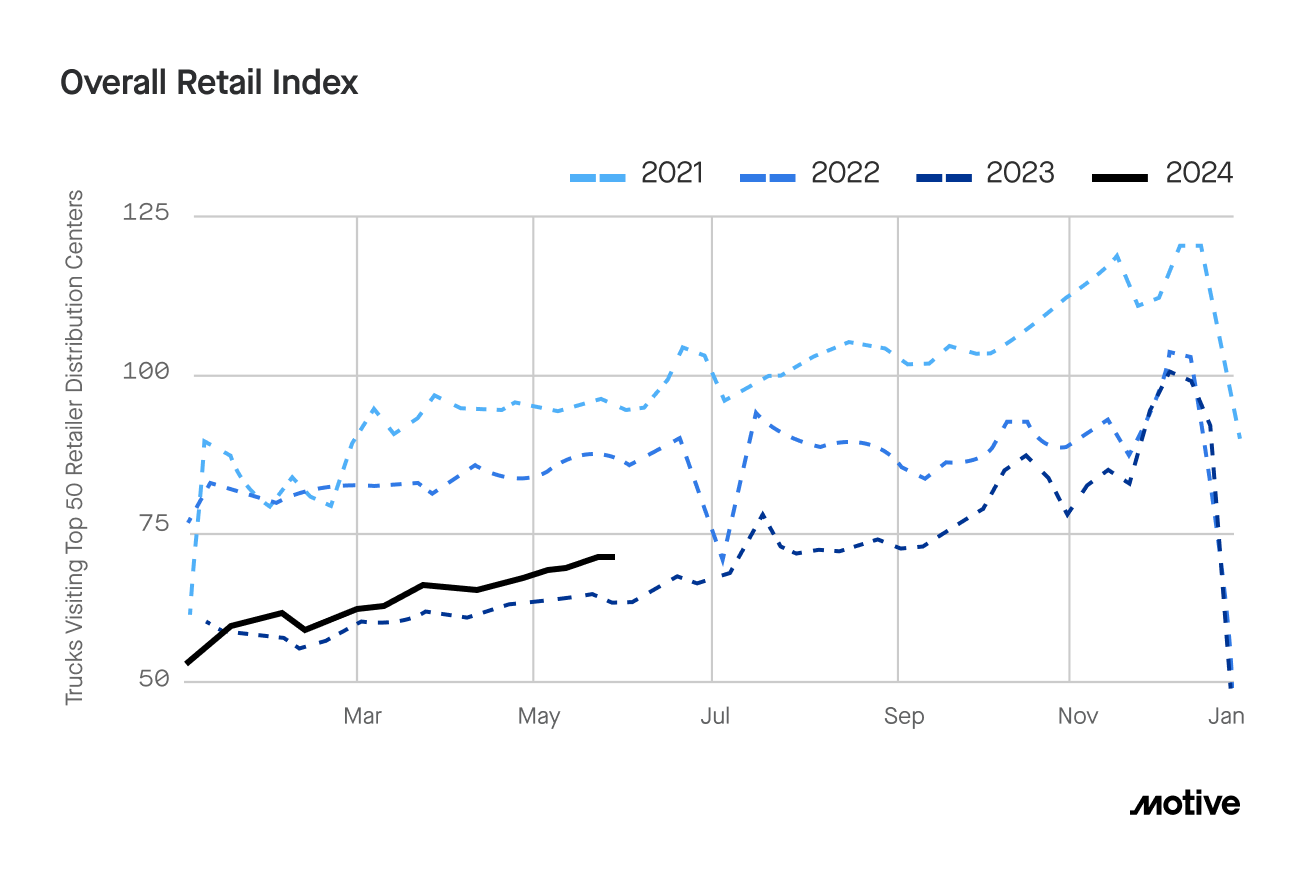

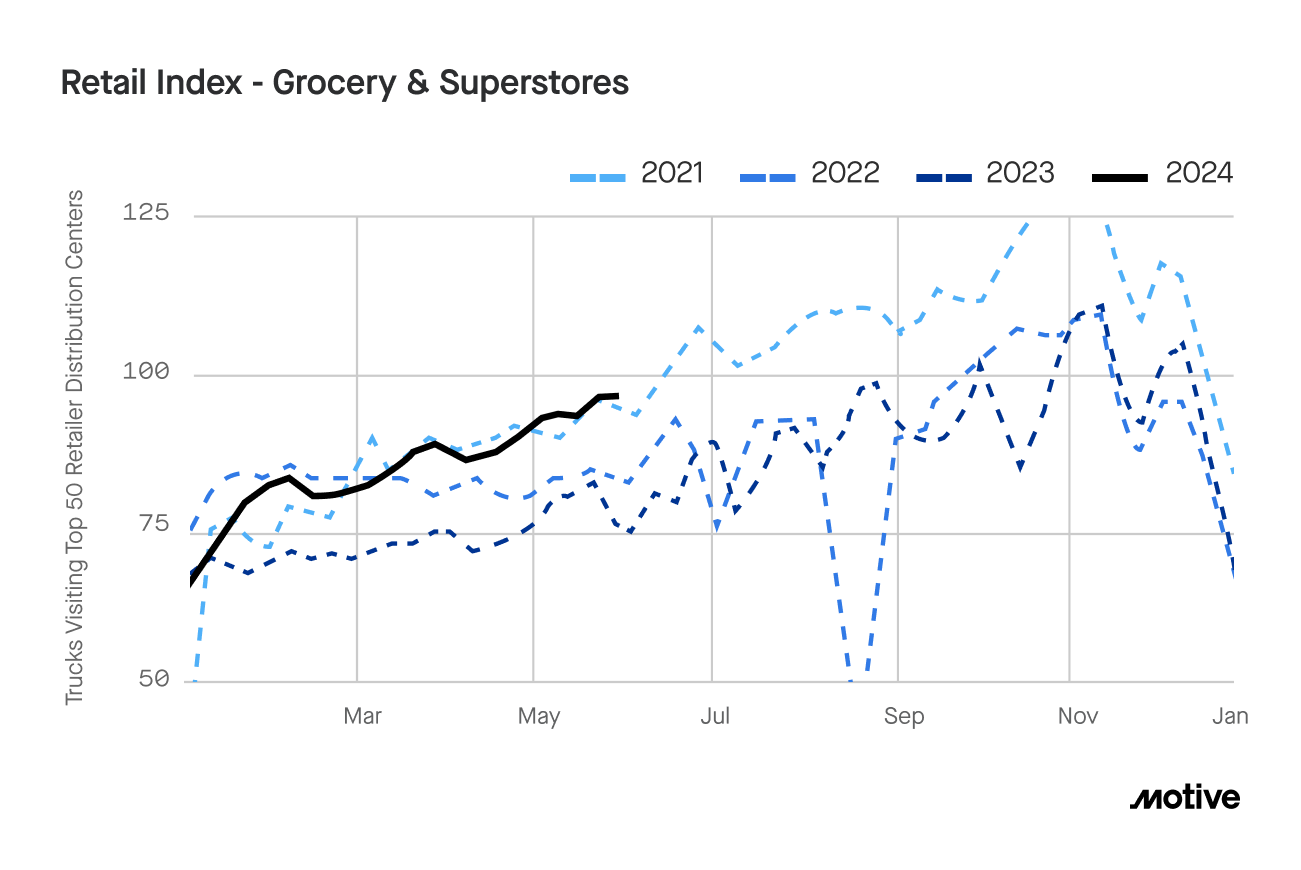

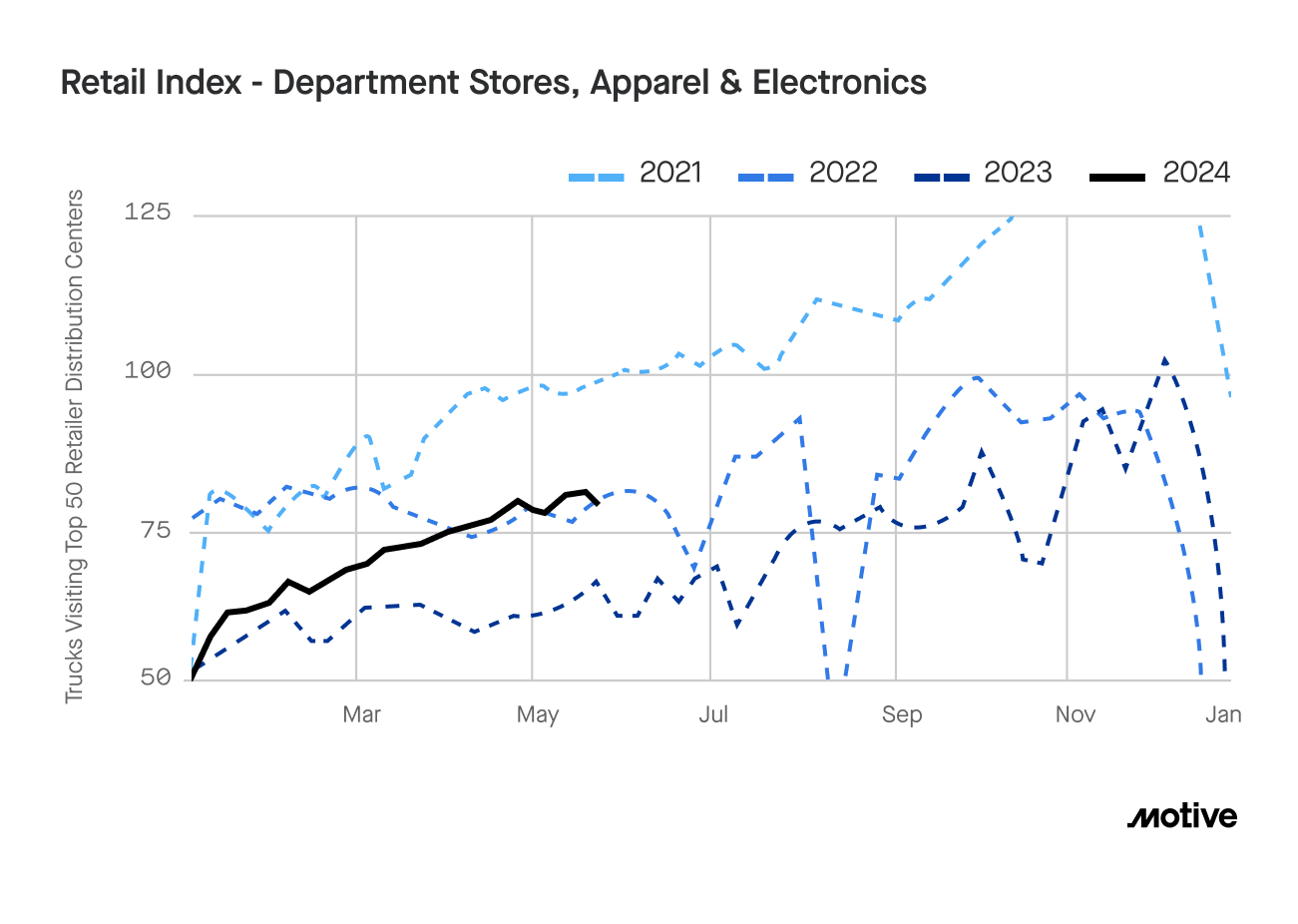

Motive’s Big Box Retail Index saw truck visits to the warehouses of the top 50 U.S. retailers jump 4% since April and 7.8% year-over-year. Significant year-over-year jumps were seen across all sectors observed, especially home improvement (+29.1%), department stores, apparel and electronics (27.7%), and grocery and superstores (22.6%). We expect these numbers to cool in June, given they were somewhat inflated by Memorial Day. However, these strong showings illustrate that retailers are well past trying to offload excess inventory and are restocking at healthy levels.

The current combination of lower rates and higher capacity has afforded these shippers both lower costs and more flexibility in moving their products. But with fewer overall carriers operating in the market, the per-mile rates to move goods will rise and impact retailer and shipper bottom lines and flexibility via the spot market. This dynamic is already underway for ocean carriers, and the trucking market will see a similar landscape later in the year. With consumers spending less in the current economic environment, retailers will need to absorb these financial impacts to keep prices low and demand high. Inevitably, however, they will need to start passing these costs to consumers.

Motive predicts that by the end of 2024/Q1 2025, retailer profitability will be hindered by rising rates, while carriers will see profitability rise. Resultant consumer price increases are expected by Q2 2025.

Higher shipping rates mean many retailers will need to rethink lean restocking.

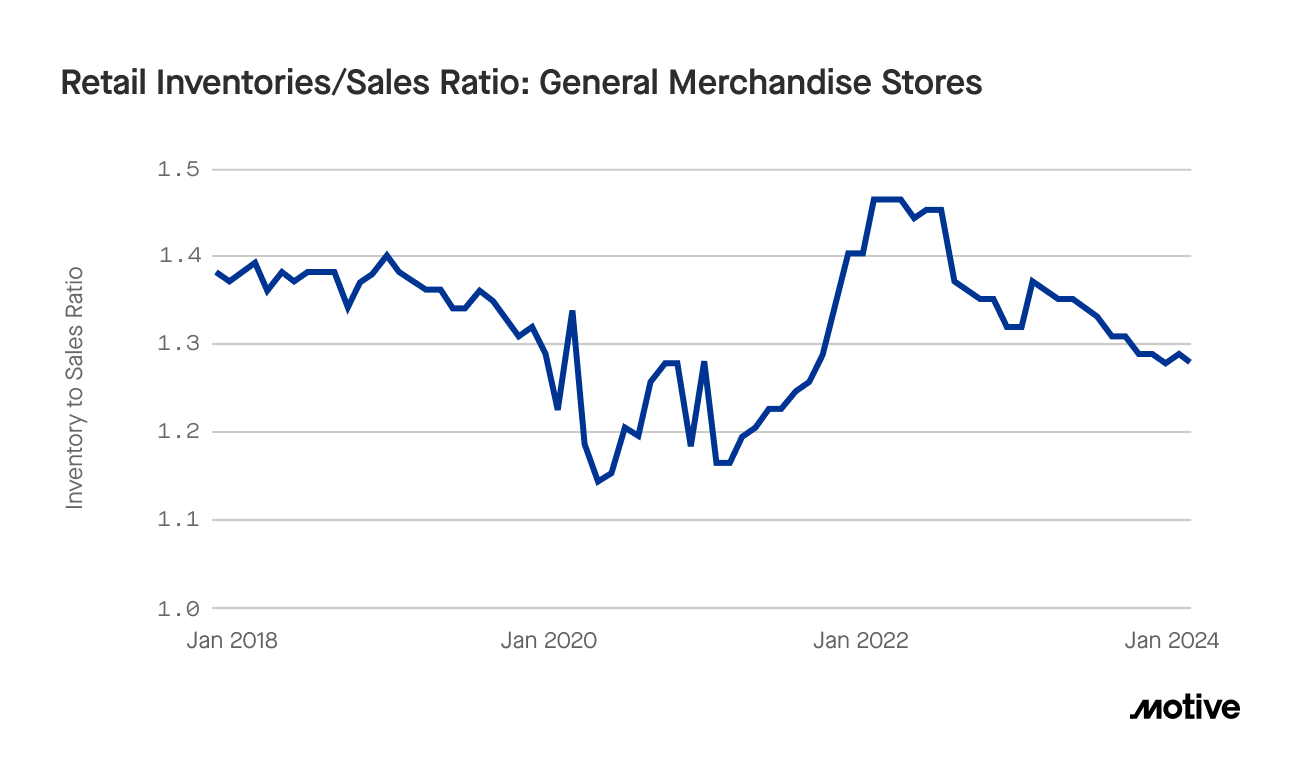

Though demand has trended upward for several months, retailer-to-sales inventory levels have stabilized at 1.3 after gradually decreasing from post-pandemic highs in March 2022. This indicates that retailers are operating with less inventory and an overall leaner resticking model, bringing inventory in closer to when they are selling it.

But how will retailers react to the aforementioned price increase taking hold and affecting their bottom line? They’ll have to make a choice: do we bring more inventory in early before the prices spike later in the year, or do we continue to operate “lean” inventories and maintain flexibility in case demand falls off? For non-durable sectors like department stores, apparel, and electronics, this will be a particularly tough choice and will require very accurate projections of what demand will look like through peak season and into Q1 of next year.

Motive predicts significant volatility in inventory levels and overall profitability in the department store, apparel, and electronics sectors in Q4 2024 and Q1 2025.

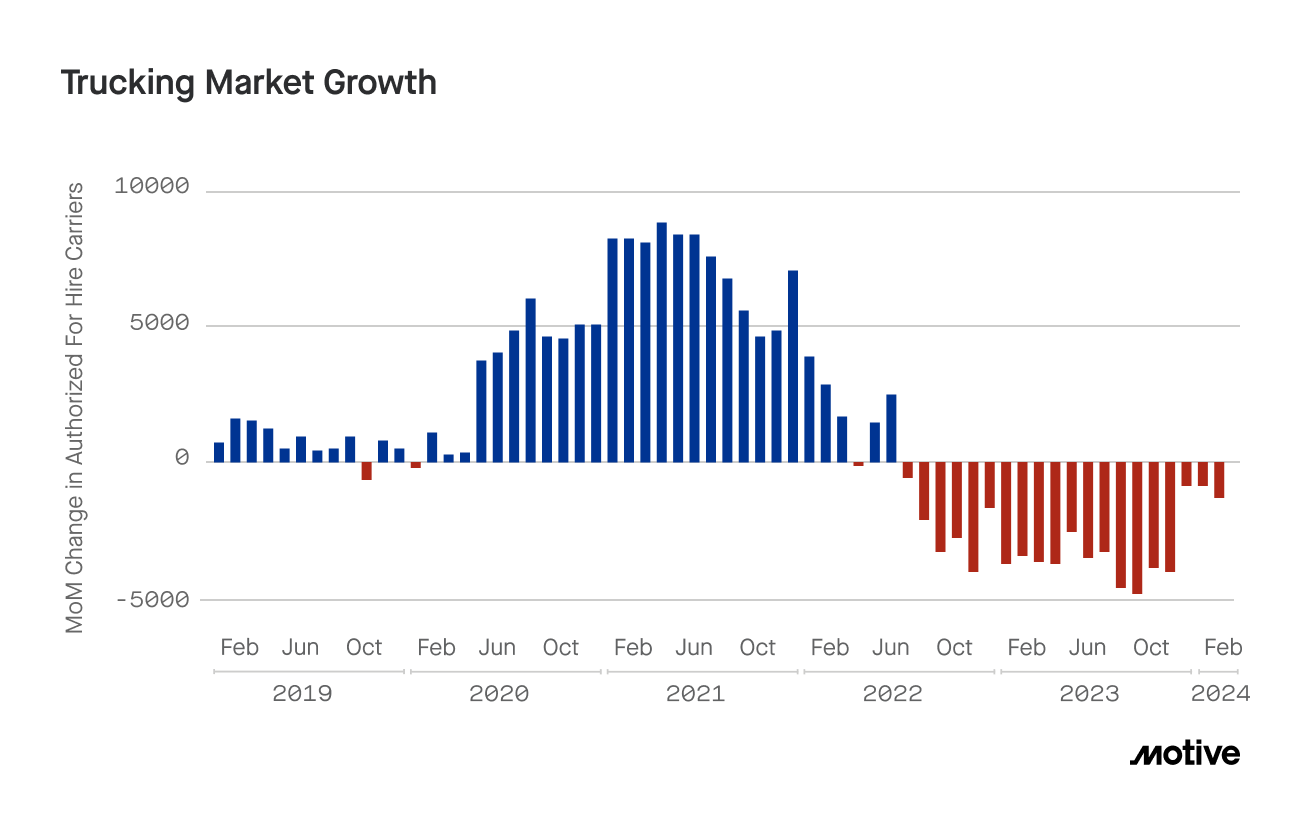

May trucking and logistics market growth remained stable and moved closer to positive growth, suggesting that trucking jobs will see an upswing by the end of the year.

1,229 trucking companies exited the market in May, representing a slight increase from March but coming in 67% lower than January. May marked the third consecutive month with fewer than 2,000 exits, indicating that market contraction continues to stabilize and move toward positive growth.

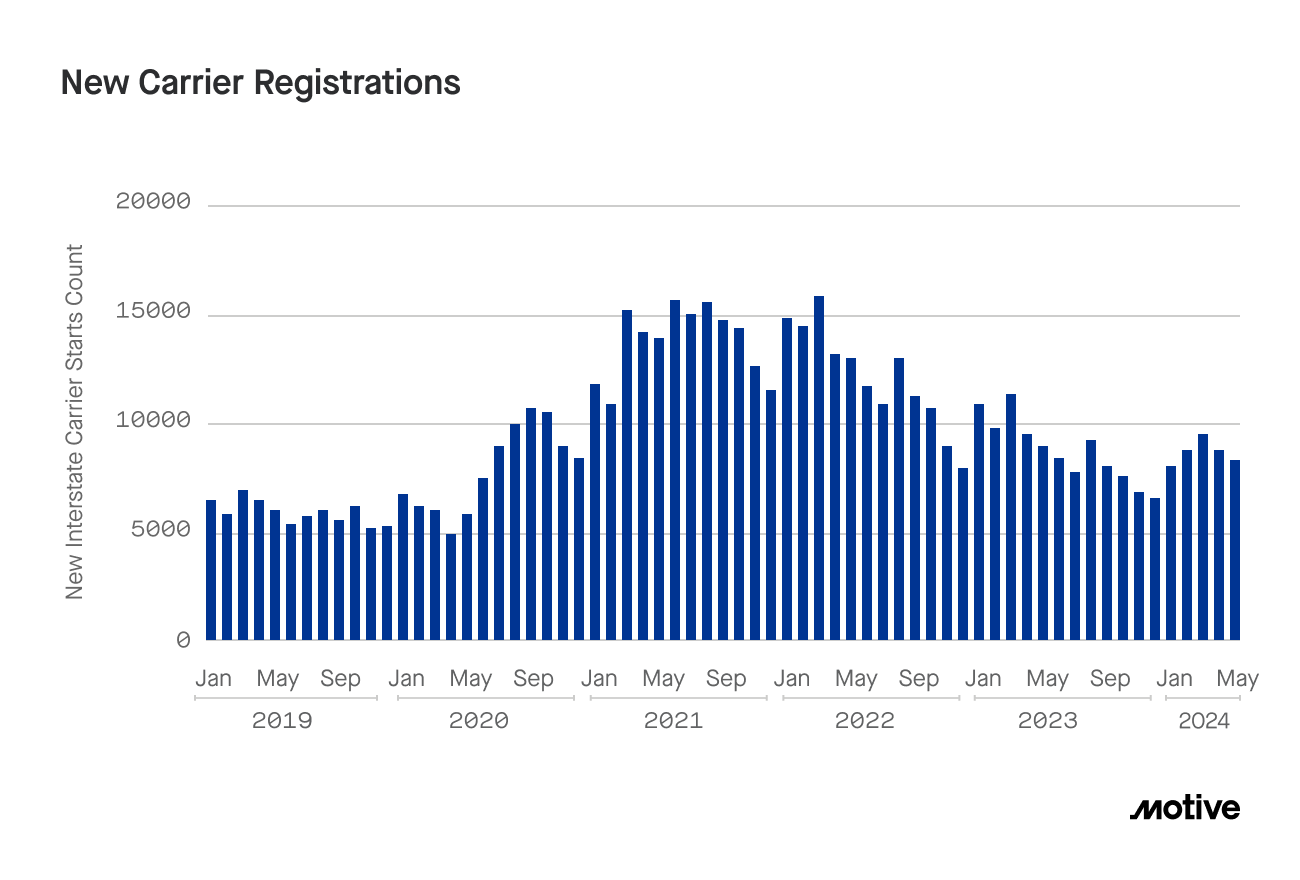

New carrier registrations told a similar story, as May saw 8,466 companies registered. While this represents a drop of 3.6% compared to April, it is also the fourth consecutive month with over 8,000 new market entrants. A total of 43,311 new carriers entered the market in 2024, compared to 31,754 over the same period in 2019, marking the recovery of this metric from the boom-bust cycle caused by the pandemic. While trucking jobs in May have trended downward, this data, coupled with coming price increases, indicates a high likelihood that trucking jobs will see an upswing.

Motive maintains its prediction that positive carrier growth will occur in the next three months of 2024 and that trucking jobs will climb significantly by the end of the year.

Higher rates may be coming, but don’t assume automatic profitability.

This month’s report highlights a shifting market that will eventually be much more favorable for carriers. However, it’s important to acknowledge that, like all trends, there is a lot of nuance, and a completely positive outlook for carriers isn’t guaranteed. Demand, for example, could go down as consumers feel further inflationary pressure. A key supply chain disruption could mean huge challenges for carriers in the affected region (or downstream effects). And the same inflationary pressure felt by retailers and consumers is also impacting carriers. This amplifies the importance of operating lean and efficiently. Carriers must carefully monitor factors like consumer demand and costs related to safety incidents and inputs like fuel to best navigate the current climate, and take advantage of future opportunities.

Data Methodology

The Motive Monthly Economic Report uses aggregated and anonymized insights from the Motive network and publicly available government data from the Federal Motor Carrier Safety Administration, U.S. Census, and U.S. Department of Transportation.