You’ve heard about IFTA but the details are complicated.

We’ll go over:

- What is IFTA?

- How does IFTA work?

- Who needs to file IFTA fuel tax?

- How to do IFTA, i.e., how to calculate IFTA fuel tax reports

- How to simplify IFTA calculation with fleet management software

Stay in business and on the right side of the law. Adhere to a number of rules and regulations that govern the roads.

Compliance is a responsibility most carriers pass on to their fleet managers. This includes licensing, USDOT numbering, hours of service rules, material regulations, and the International Fuel Tax Agreement (IFTA).

Fleet managers ensure the company follows compliance rules. But awareness of the regulations can help drivers and carriers make better-informed decisions to benefit their fleet.

IFTA is an often confusing regulation, so before we get deep into the details, let’s start by answering two questions: what is IFTA, and how does it work?

What is IFTA?

IFTA is the cooperative agreement between 48 states in the U.S. and 10 provinces in Canada. It allows inter-jurisdictional carriers to report and pay taxes for the fuel their vehicles consume across states. Using a single fuel tax license.

To fully understand IFTA, it’s important to know why the agreement was made in the first place.

Prior to IFTA, truckers were required to obtain fuel permits from every state they entered.

Not only was the process inefficient, but it also meant additional costs in the form of lost time, fuel burned en route to permit purchasing centers, and the applicable fees.

Fleets also had to comply with inconsistent filing periods, rules, definitions, and reporting requirements that involved hours of clerical work.

IFTA has improved efficiency in fuel tax payments among member states. According to estimates, it saves trucking businesses millions of dollars annually in administrative costs.

Here’s a list of the states and provinces that are members of the IFTA agreement:

Canada

- Alberta

- British Columbia

- Manitoba

- New Brunswick

- Newfoundland

- Nova Scotia

- Ontario

- Prince Edward Island

- Quebec

- Saskatchewan

United States of America

- All states except for Alaska, Hawaii, and the District of Columbia

How IFTA works

Apart from the benefits of IFTA to trucking businesses, the agreement also makes sure jurisdictions are properly compensated for the use of their roads by heavy commercial vehicles.

Under IFTA, carriers only need to report inter-jurisdictional fuel use to their base state. The state will collect the taxes on net fuel use, process fuel tax returns, and distribute the funds to all the other states.

The base state is also responsible for enforcing compliance through scheduled audits.

Who needs IFTA?

Carriers need an IFTA license if they’re based in a member state and operate across two or more member jurisdictions. Another consideration is the type of vehicle they use.

IFTA defines a qualified motor vehicle as a vehicle built and used to transport property or people. Qualified motor vehicles must also fit any of the following descriptions:

- Any vehicle with two axles and a gross vehicle weight of over 11,797 kilograms or 26,000 pounds

- A vehicle of any weight but with three or more axles

- A vehicle that exceeds 11,797 kilograms or 26,000 pounds

Applying for an IFTA license and decals

If you need an IFTA license, the first step is to fill out the application form used in your base state.

Application forms may vary and can sometimes serve other purposes. For example, carriers based in Ohio can use the IFTA application form to request additional decals or make changes to their account.

Some of the basic carrier information required for new IFTA applications are:

- Registered business name

- Mailing address

- Federal business number

- USDOT number

If downloaded online, completed IFTA forms can be sent by mail. Other jurisdictions also allow IFTA forms to be sent by fax or through taxpayer service offices.

Once your application has been processed, the IFTA authority in your state will issue official IFTA decals for the current year. A temporary IFTA license can be faxed to you while you wait for your decals.

Filing quarterly IFTA taxes

The next step is to figure out how much IFTA is going to cost your fleet.

An IFTA licensee’s primary objective is to file a quarterly return with their base state.

IFTA quarters

Below is a list of the IFTA return due dates for each reporting quarter:

- 1st quarter (January to March) — April 30

- 2nd quarter (April to June) — July 31

- 3rd quarter (July to September) — October 31

- 4th quarter (October to December) — January 31

Late payment fees will be incurred if you pay after the IFTA quarters deadlines.

How to calculate IFTA fuel tax reports?

Now the main question: How do you do IFTA?

IFTA tax calculations can be summarized in five simple steps:

1. Tracking miles you’ve traveled in each state

Fleet managers and drivers must work together to accurately record the amount of fuel consumed in different jurisdictions. This requires fleets to be extremely organized with how they handle their drivers’ records of duty status.

Drivers must also do their part and diligently record their odometer readings whenever they cross state lines. To avoid human error, you can use route planning or fleet management software to digitally log the miles your drivers cover for each jurisdiction.

2. Adding fuel purchases

The next piece of information you need for IFTA fuel tax reports is the total gallons of fuel purchased in each jurisdiction.

Remember, carriers must retain the original receipts or invoices to prove that fuel tax was paid. These documents must contain:

- Fuel purchase date

- Fuel seller’s name and location

- Type of fuel purchased

- Vehicle plate number

- Number of gallons purchased

- Price per gallon

- Driver’s name

3. Calculating fuel consumed per state

Once you have the total miles and fuel purchased tallied, it’s time to calculate the fuel mileage of your vehicles for each jurisdiction. You can use the simple formula below to calculate your fleet’s overall fuel mileage:

Total miles driven / Total gallons = Overall fuel mileage

For example, if you purchased a total of 4,000 gallons of fuel and covered 22,000 miles, then your overall fuel mileage would be:

22,000 / 4,000 = 5.5 miles per gallon

Be sure to round off the MPG value to two decimal places.

To calculate how many gallons your fleet consumed in each jurisdiction, input your overall fuel mileage to the formula below:

Total miles driven in State X / Overall fuel mileage = Fuel consumed in State X

Use the second equation for each state or province you operated in during the current reporting period.

4. Calculating taxes owed for each state and province

The fuel purchased per jurisdiction is the key metric needed to calculate the fuel tax amount your fleet owes each jurisdiction. This is dependent on the applicable rates during the current IFTA quarter.

You can view the complete chart of fuel tax rates for each fuel type and jurisdiction on the International Fuel Tax Association website. Take note that these rates are subject to change until the next due date. You don’t have to perform this calculation until then.

5. Putting it all together

Finally, you can use the formula below to calculate the actual tax amount you owe each state.

Fuel tax required in State X – Fuel tax paid in State X = Fuel tax owed to State X

You can determine the amount of fuel tax paid upon purchase from fuel receipts or fuel withdrawal slips.

Things to remember

The formulas above skip certain aspects of IFTA tax reporting. Be prepared to make adjustments. Especially once fuel tax rates are finalized at the end of every IFTA quarter.

Some of the important elements you should remember when filing quarterly IFTA taxes are:

Taxable miles

Your fleet’s total taxable miles is usually the same as the total miles driven in each jurisdiction. However, certain jurisdictions allow mileage exceptions that don’t count as taxable. Such as fuel trip permit miles.

Taxable gallons consumed

To calculate your vehicle’s taxable gallons consumed, divide your total taxable miles by your overall fuel mileage. You can then subtract your total tax for paid gallons purchased to get your net taxable gallons.

Surcharges

Surcharges allow a state where fuel is purchased to keep a portion of the money regardless of where the fuel is used. Fleets should only purchase the amount of fuel they expect to use within jurisdictions where surcharges apply.

Using ELDs and fleet management software for IFTA calculation

Traditionally, drivers and fleet managers had to manually track their vehicle miles and fuel purchases when filing quarterly IFTA taxes. Everything must be accounted for. From fuel purchase receipts to a list of miles driven in each jurisdiction.

Drivers can use the tax reporting worksheet from the Owner-Operator Independent Drivers Association (OOIDA) to keep track of their fuel purchases, miles driven, jurisdictions, and routes traveled.

Alternatively, they can turn to cloud-based reporting tools and fleet management software with IFTA reporting features.

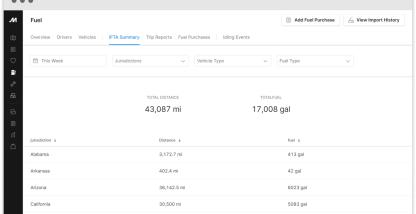

Motive offers an IFTA reporting feature that empowers you to automatically monitor and sorts your vehicle’s fuel purchases, utilization, and costs for each jurisdiction.

There are two ways to import fuel purchase data.

The first method is to upload a CSV file from your fleet’s fuel card vendor via the Motive web dashboard. Secondly, drivers can manually submit their fuel purchases as well as upload photos of fuel receipts from the Motive App.

For more information, read How to prepare IFTA reports in just a few clicks.

We recently updated our IFTA feature Now, it’s easier for drivers to upload fuel purchases directly to the Motive dashboard. This allows you to make bulk imports from major fuel cards. In other words, you can import all of your receipts at once.

Try the Motive ELD solution by clicking the following image. See how Motive simplifies IFTA reporting.

IFTA FAQs

Filing quarterly IFTA taxes can be a challenge. Even with all the tools that can expedite reporting. To make your job more manageable, here’s a short roundup of frequently asked questions about IFTA.

Do I need to file IFTA taxes if I didn’t move any freight?

Yes. Filing quarterly IFTA taxes is required even if your fleet was inactive during the reporting period.

What if we never went beyond our base state for the entire quarter?

You’re still required to file your quarterly IFTA report even if you didn’t operate outside your jurisdiction for a given quarter.

How can my fleet get new IFTA decals?

New decals will be supplied to your fleet whenever you renew your IFTA license, which is done annually. If you lose or damage your IFTA decals, you can send a request to your jurisdiction’s IFTA authority and order new ones.

What if an intrastate fleet is suddenly required to operate out of state?

For one-time trips between two or more jurisdictions, fleets can use temporary trip permits. These are only valid for one vehicle on a specific journey into another jurisdiction.

To acquire a single-trip permit, the carrier must define the time period and total distance to be covered. This information will be used to calculate the fuel tax to be paid along with other applicable fees.

What are the penalties for failing to file or pay an IFTA quarterly return?

If a carrier fails to file a quarterly IFTA return, they have 30 days to complete the requirements before their license gets suspended.

Late payments are subject to a penalty of $50 or 10% of the total tax due. Whichever is higher.

Simplify IFTA reporting with modern technology

Fuel tax preparation can be tedious. But once you fully understand the ins and outs of IFTA, it’ll be easier to tackle.

IFTA eliminates the messy fuel tax reporting practices of old. It also enables jurisdictions to fund road repairs and improvements, which directly impacts the safety of commercial fleets on the road.

Although IFTA fuel tax calculation and reporting can be overwhelming, you can use the Motive fleet management solution to simplify the process.

For more details, read how you can easily calculate IFTA fuel tax with Motive.